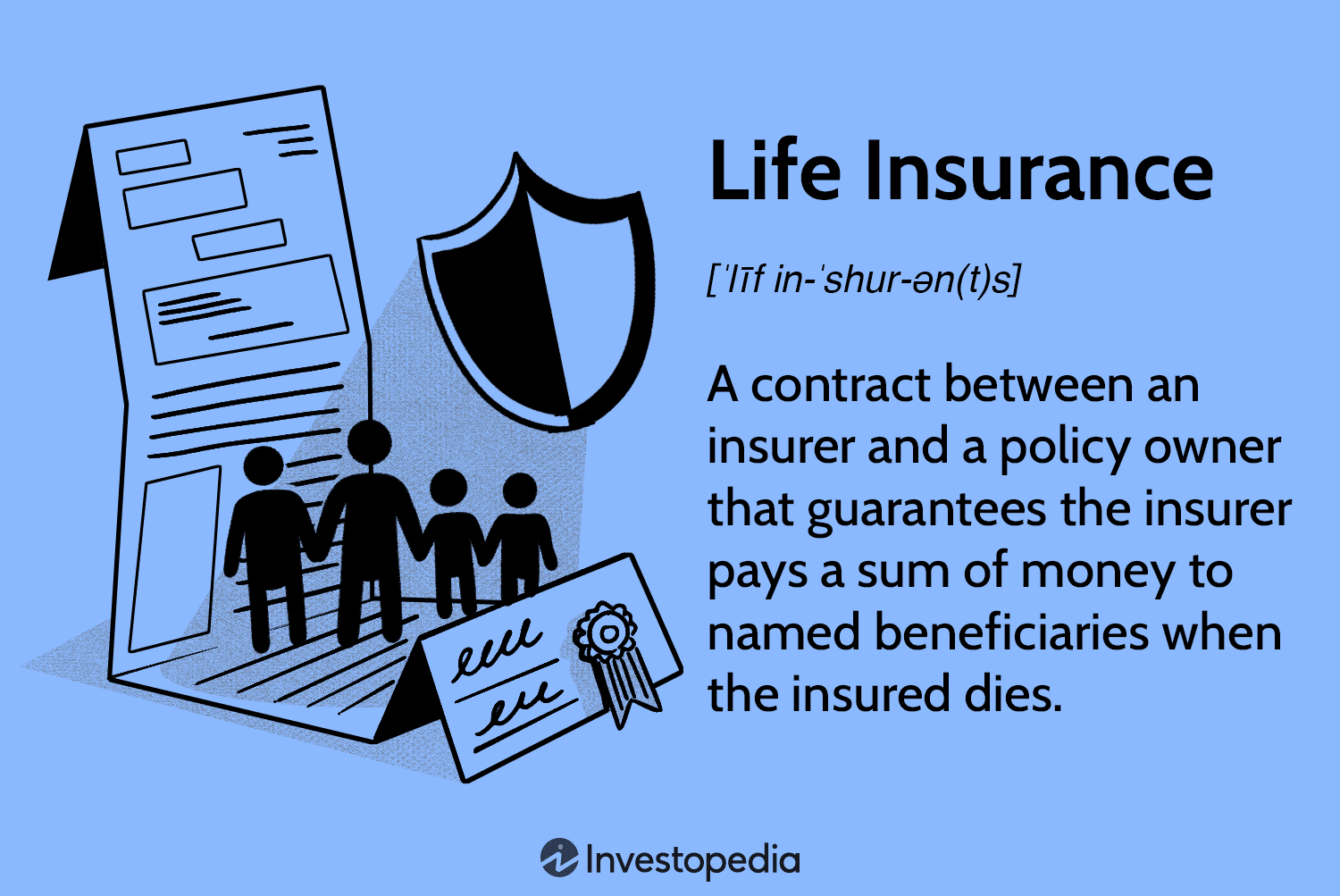

Understanding how disaster protection functions and how to look for a strategy can assist you with tracking down the best inclusion to address your family’s issues. Disaster protection is an agreement between an insurance agency and a strategy proprietor wherein the safety net provider certifies to pay an amount of cash to at least one named recipient when the guaranteed individual kicks the bucket.

In return, the policyholder pays charges to the safety net provider during their lifetime. The best disaster protection organizations have great monetary strength, a low number of client grumblings, high consumer loyalty, a few accessible strategy types, discretionary riders, and simple application processes.

Types of Life Insurance

Many kinds of extra security are accessible to meet a wide range of buyer needs and inclinations. Contingent upon the short- or haul needs of the individual to be protected (or their relatives), deciding whether to choose brief or extremely durable life coverage will be a significant thought.

Term life insurance

Term extra security is intended to last a specific number of years, then end. You pick the term when you take out the approach. Normal terms are 10, 20, or 30 years. The best-term extra security strategies balance moderateness with long-haul monetary strength.Level term, the most widely recognized sort of term insurance right now being sold, pays a similar measure of death benefit all through the contract’s term.

Different kinds of term protection include:Diminishing term life coverage is sustainable term extra security with inclusion that reductions over the existence of the strategy at a foreordained rate.Convertible term disaster protection permits policyholders to switch a term strategy over completely to long-lasting protection.nexhaustible term life coverage states the year the strategy is bought. Expenses increment every year at reestablishment. These plans normally give the most affordable term protection in the main year.

Permanent Life Insurance

Super durable life coverage is more costly than term, however, it stays in force all through the guaranteed’s whole life except if the policyholder quits paying the charges or gives up the strategy. A few strategies take into consideration programmed premium credits when an exceptional installment is overdue.2

Entire extra security is one sort of long-lasting disaster protection where the premium and demise benefits for the most part continue as before every year. It incorporates a money esteem part, which is like a bank account. Cash-esteem life coverage permits the policyholder to involve the money as an incentive for some reasons, for example, to take out advances or to pay strategy expenses.

General life (UL) protection is one more sort of long-lasting extra security with a money esteem part that procures revenue. General life highlights adaptable charges. In contrast to term and entire life, charges can be changed over the long run. UL likewise lets the policy owner pick between level demise benefit or expanding passing advantage choices.

Term vs. Permanent Life Insurance

Term extra security contrasts from super durable life coverage. In more than one way however will in general best address the issues of the vast majority searching for reasonable disaster protection inclusion. Term disaster protection just goes on for a set timeframe and pays a demise advantage should the policyholder bite the dust before the term has lapsed. That is rather than extremely durable life coverage, which stays in actuality as long as the policyholder pays the premium. Another basic contrast includes charges: term life is for the most part considerably less costly than extremely durable life since it doesn’t gather cash esteem.

For instance

assuming that you are the essential overseer and have kids two and four years of age, you would believe sufficient protection should cover your custodial obligations until your youngsters are developed and ready to help themselves.

You could investigate the expense of recruiting a babysitter and a maid or utilizing business kid care and cleaning administrations, then, at that point, maybe add cash for instruction. Incorporate any remaining home loan and retirement needs for your companion in your disaster protection computation — particularly if the mate procures fundamentally less or is a stay-at-home parent. Complete what these costs would be over the following 16 or so years, add somewhat more for expansion, and that is the demise benefit you should purchase — on the off chance that you can bear the cost of it.

What Affects Your Life Insurance

Many variables can influence the expense of extra security charges. Certain things might be outside of your reach, however, different measures can be figured out how to possibly cut down the expense previously (and, surprisingly, after) applying. Your well-being and age are the main factors that decide the cost, so purchasing disaster protection when you want it is much of the time the best strategy.

In the wake of being supported for an insurance contract, if your well-being works out later and you’ve made a positive way of life transforms you can request to be considered for an adjustment of chance class. Regardless of whether tracked down, you’re in less fortunate well-being than at the underlying endorsing, your charges won’t go up. If you’re viewed as in better well-being, your expenses might diminish. You may likewise have the option to purchase extra inclusion at a lower rate than you at first did.

Life Insurance Buying Guide

Believe about what costs should be shrouded in case of your passing. Consider things, for example, contracts, schooling costs, charge cards, different obligations, also burial service costs. Likewise, pay substitution is a central point on the off chance that your mate or friends and family will require income and can’t give it all alone.

Disaster protection applications

for the most part require individual and family clinical history and recipient data. You might have to take a clinical test and should unveil any previous ailments, history of moving infringement, DUIs, and any hazardous side interests, (for example, auto dashing or skydiving). Coming up next are vital components of most disaster protection applications:

Standard types of distinguishing proof will likewise be required before a strategy can be composed, for example, your Government-managed retirement card, driver’s permit, or U.S. visa.

Look at Strategy Statements

Whenever you’ve collected the entirety of your important data, you can accumulate numerous life coverage quotes from various suppliers given your examination. Costs can contrast notably from one organization to another, so it means a lot to put forth the attempt to find the best mix of strategy, organization rating, and premium expense. Since extra security expenses are something you will probably pay month to month for quite a long time, finding the strategy that best meets your requirements can save you a huge measure of cash.

Our setup of all that life coverage organizations can kick you off on your examination. It records the organizations we’ve viewed as the best for various sorts of requirements, in light of our examination of almost 100 transporters.

Advantages of Life coverage

There are many advantages to having disaster protection. The following are the absolute most significant elements and securities presented by life coverage approaches.

A great many people use life coverage to give cash to recipients who might experience monetary difficulty upon the protection’s demise. Be that as it may, for rich people, the expense benefits of extra security, including the duty conceded development of money esteem, tax-exempt profits, and tax-exempt passing advantages, can give extra essential open doors.

Keeping away from Assessments

The demise advantage of a life coverage strategy is generally charge-free.3 It could be dependent upon home duties, however, that is the reason well-off people some of the time purchase long-lasting disaster protection inside a trust. The trust assists them with keeping away from home charges and safeguarding the worth of the domain for their main beneficiaries.